All decisions, whether it is in business, engineering, government, or personal life are based on decision-making methods. The decision about which method to use will impact all your personal and business decisions.

The figure below illustrate the importance of methods in decision-making. Methods produce decisions, which in turn guide actions, which finally lead to the outcomes. If the outcomes matter then you decision-making methods should also matter.

Cause-effect model of decision-making (Suhr 1999).

Cause-effect model of decision-making (Suhr 1999).

In fact, using different decision-making methods with the same information may lead to different outcomes. The selection of a decision-making method is very important; therefore it should not be left to chance.

The root cause of undesirable outcomes is often the use of inappropriate methods of decision-makings. Moreover, many organizations make decisions without collaborating with relevant stakeholders, which leads to suboptimal solutions, or change decisions later paying a higher cost. Organizations can benefit from a transparent and collaborative decision-making process.

Different types of decisions will require different types of decision-making methods. Roy (1974) made a classification of decisions types. These can be summarized as follows.

There are also other types of decisions described later by Belton and Stewart (2002).

Different types of methods can support these types of decisions. Multi-Criteria Decision-Making (MCDM) or Multi-Criteria Decision-Analysis (MCDA) methods help consider multiple criteria in a decision. We can categorize MCDM methods under four categories:

The first three methods are easily found in the literature about MCDM methods. For more information about MCDM or MCDA methods visit the following wikipedia page. Paramount Decisions is based on Choosing By Advantages (CBA) Tabular method. Literature about CBA method is mainly found in the Lean community. We have gathered some of the Books and Research Papers in our Decision-Making Training.

Choosing By Advantages (CBA) is a decision-making system that supports transparent and collaborative decision-making using comparisons among advantages of alternatives.

CBA was developed by Jim Suhr while working in the U.S. Forest Service. The CBA Decision-Making System is based on the idea that decisions should be based on comparative advantages among the alternatives. This idea can be explained using natural selection where one species survives because it has an advantage versus its prey (e.g., Cheetah runs 10 miles per hour faster than the rabbit). It doesn't matter how fast the rabbits runs or how fast the cheetah runs, it is their difference in speed that produces the advantage for the cheetah.

The difference between two alternatives can be viewed as positive or negative—as an advantage of the one alternative, or as a disadvantage of the other alternative. According to Suhr, decisions should be based on the Importance of Advantages (IofA), rather than advantages and disadvantages or the quantity of advantages. Traditional methods tend to count both the advantages and the disadvantages of certain alternatives and compare the quantity of advantages to the quantity of disadvantages. However, when they list all the advantages of a specific alternative over another alternative, they essentially list all the disadvantages of the latter compared to the former, and vice versa. So by also making extra lists for the disadvantages of each alternative, they are double-counting the differences. Suhr characterizes double–counting as a “critical mistake”. Traditional methods tend also to select alternatives that have the most advantages rather than the most important advantages, leading to suboptimal solutions and outcomes.

In addition, decisions should be anchored to the relevant facts. Traditional methods tend to base decisions on generalities, without clear and specific meanings. CBA require specific and clear criteria, consistent measurement methods, and correct data to be used. For example, when choosing a construction method could you say that productivity is more important than safety? Or that safety is more important than productivity? These are question that lead to an endless and useless argumentations process that says nothing about the real alternatives that are available for choosing. CBA is based on understanding what are the advantages of one alternative over another and then based on actual advantages decision-makers assess the importance of those advantages. In this way, CBA postpones the value judgment and anchors decisions to relevant facts.

CBA also helps decision makers to separate cost from value. The influence of cost is very high in personal and corporate decisions. However, many alternatives are not even explore to understand the value they provide. These is especially true when it comes to sustainability decisions. In CBA, the alternatives are analyzed comparing the advantages of one another and at the end decision makers include the cost analysis with the first and lifecycle cost of the alternatives.

According to Suhr, “The CBA skills are as basic and as essential as reading and writing. And like reading and writing skills, they are not acquired naturally.” Therefore, CBA requires training to educate decision makers. Training and practicing is essential in this matter. According to Koga (2005), “like learning a musical instrument, daily practice is essential”.

Finally, CBA is not only one method, but a system of methods for sound decisions making. According to Suhr, “Different types of decisions call for different sound methods of decision-making.” The CBA decision-making system provides therefore a system of methods to help the decision maker to arrive at a sound decision. The CBA decision-making system can be developed for decisions ranging from very simple to very complex. The CBA methods can be used for prioritizing proposals or projects, and for choosing among two alternatives, multiple alternatives, or a large number of alternatives.

To better understand why CBA is superior to other methods visit our Blog or our collection of peer reviewed research papers.

CBA defines its own vocabulary, urging people who use the system to all speak in the language in order to foster clarity. According to Suhr (1999), anyone who is not using “the sound decision-making vocabulary” is not using CBA.

Specific meanings have been given to the terms alternative, factor, criterion, attribute and advantage and their definitions are provided below.

As defined above, a ‘factor’ is a component of a decision. Acting like a container, a factor could also be compared to an underlined heading preceding a set of sentences. A factor contains criteria (decision-rules), attributes (the specific characteristic of each alternative within this factor), and advantages (the result of comparing only two attributes at one time). Each term conveys an aspect giving meaning to the factor within a context.

A criterion may be a ‘must’ criterion, representing conditions that have to be satisfied, or ‘want’ criterion, representing preferences of one or multiple stakeholders. If an attribute of an alternative does not meet a ‘must’ criterion, the alternative is eliminated and no longer considered.

While an attribute is a characteristic of just one alternative, an advantage is a difference between the attributes of two alternatives. Only advantages are expressed in the CBA system and no disadvantages are considered. According to Suhr (2012), a disadvantage of one alternative is an advantage of another alternative. And, there are no exceptions. As follows, there are differences only in the ways we view them and name them.

CBA is centered on several principles that are applied in all the methods. According to Suhr (2012), there are several principles that ensure sound decision-making and that constitute the foundations of CBA. Some of the CBA principles are:

The first principle rules out all methods that fail to base decisions on the importance of differences. Suhr (2012) characterize the traditional decision-making methods that base their decisions on specific factors and criteria, and then weigh these factors and criteria to make the final decisions for “unsound methods that cause critical mistakes and cause conflicts”. Sound methods should base the decisions on the importance of the differences between the alternatives, instead of the factors, criteria, attributes, goals, roles, categories, objectives, pros and cons, and so forth.

The difference between two alternatives can be viewed as positive or negative—as an advantage of the one alternative, or as a disadvantage of the other alternative. Sound methods should base their decisions on the Importance of Advantages (IoA), rather than advantages and disadvantages or the quantity of advantages. Traditional methods tend to count both the advantages and the disadvantages of certain alternatives and compare the quantity of advantages to the quantity of disadvantages. However, when they list all the advantages of a specific alternative over another alternative, they essentially list all the disadvantages of the latter compared to the former, and vice versa. So by also making extra lists for the disadvantages of each alternative, they are double-counting the differences. Suhr characterizes double–counting as a “critical mistake”. Traditional methods tend also to select alternatives that have the most advantages rather than the most important advantages, leading to suboptimal solutions and outcomes.

In addition, sound decisions should be anchored to the relevant facts. Traditional methods tend to base decisions on generalities, without clear and specific meanings. CBA require specific and clear criteria, consistent measurement methods, and correct data to be used. In this way, CBA also postpones the value judgment until those criteria are met.

Also, decision makers need to learn how to use sound methods. According to Suhr (2012), “The CBA skills are as basic and as essential as reading and writing. And like reading and writing skills, they are not acquired naturally.” The fourth principle of CBA is based on the concepts of learning and teaching step-by-step, and introducing sound decision-making to the educational systems and to the industry. In addition to learning, the decision makers must skillfully use the sound methods of decision-making. Training and practicing is essential in this matter. According to Koga (2005), “like learning a musical instrument, daily practice is essential”.

Finally, Different types of decisions call for different types of methods. Some of the methods in CBA simplify simple decisions by taking fewer steps (e.g. instant CBA), while other simplify complex decisions by take smaller steps ( e.g. Tabular Method). Paramount Decisions helps simplify complex decisions, and is based on CBA Tabular Method.

CBA simplifies complex decision-making by dividing it into five phases:

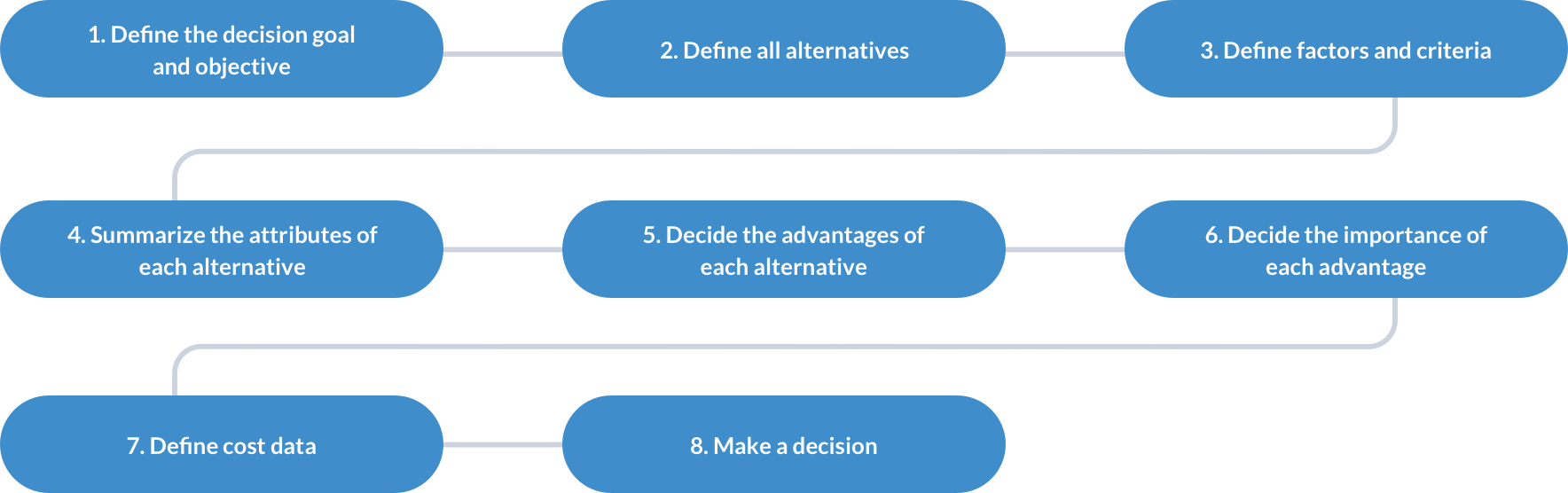

Each phase is further divided into small steps, and there are CBA methods for each phase of the decision-making process. Paramount Decisions is based on the Tabular Method of CBA that can be used in both simple and complex decisions. The Tabular Method can be described in 7 steps:

CBA Steps (Adopted from Arroyo, Tommelein and Ballard 2013)

CBA Steps (Adopted from Arroyo, Tommelein and Ballard 2013)

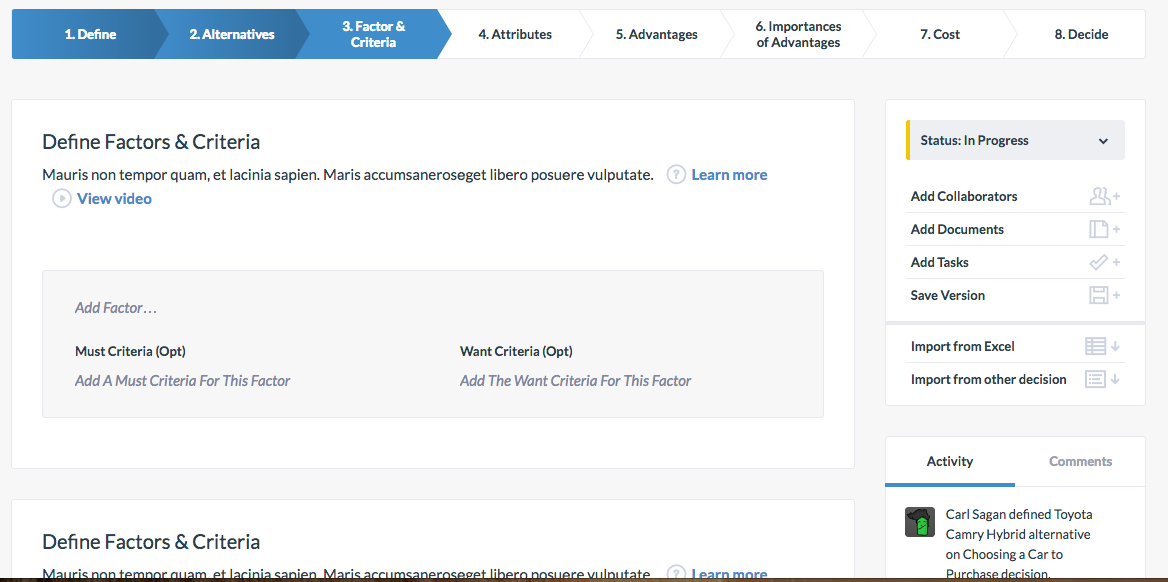

To begin the decision-making process, the stakeholders identify alternatives likely to yield important advantages over other alternatives and that reflect values the team wants to realize in their design solutions (Step 1). They also have to define factors to evaluate attributes of alternatives (Step 2), and agree on the criteria for each factor (Step 3). Criteria can be either a desirable (‘want’) or a mandatory (‘must’) decision rule. Alternatives that do not comply with a ‘must’ criterion are not considered in the following steps.

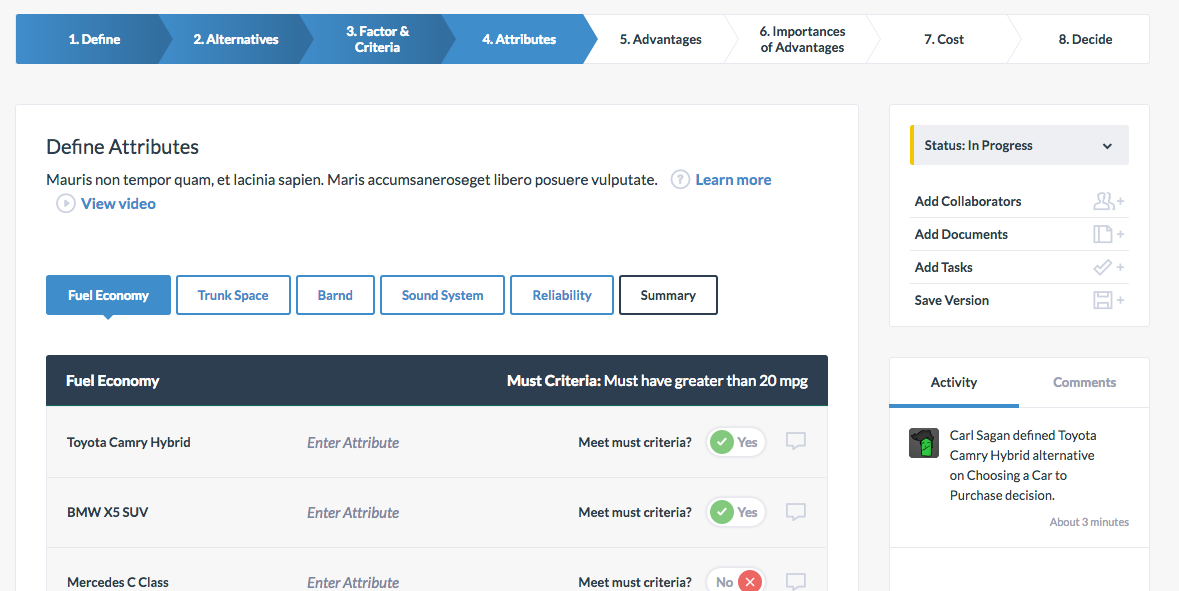

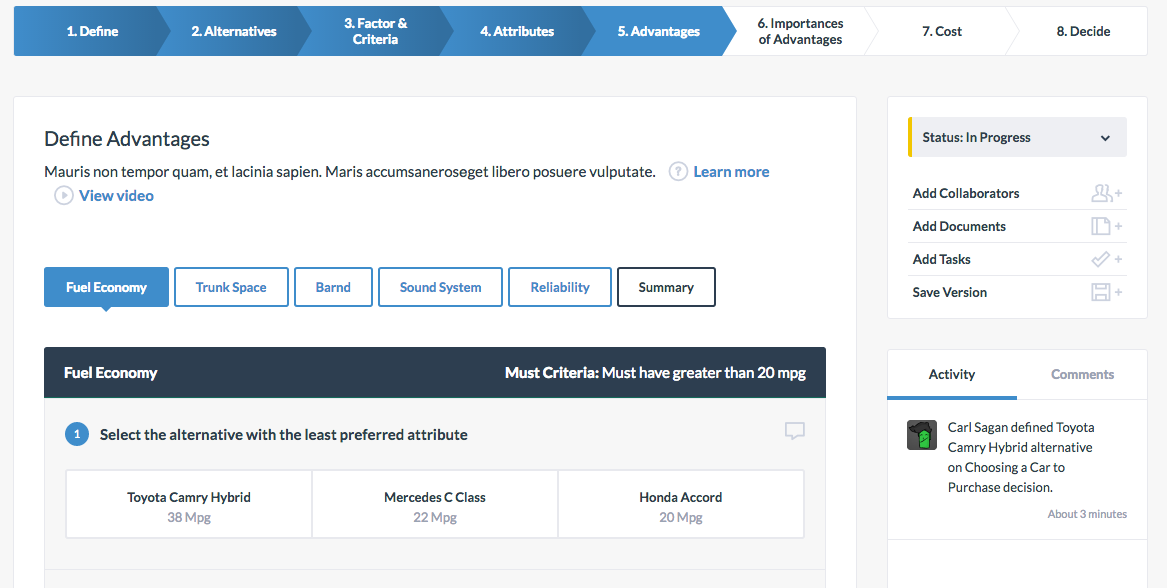

After identifying the alternatives and defining the factors and criteria, the stakeholders summarize the attributes of each alternative (Step 4). Summarizing attributes consists of listing objective facts or data to describe the attributes of each alternative, corresponding to the factors and criteria shown, thus anchoring the decision-making process to relevant facts. Attributes are inherent to an alternative, so this step avoids subjective judgment. Repeating row by row, for each ‘want’ criterion, the team then determines which alternative has the least preferred attribute and underlines it.

The next step is to determine the advantages of each alternative (Step 5). This is done by comparing each attribute to the least preferred attribute in each factor. Determining the advantages of each alternative depends on the criteria that pertain to a given factor, but does not require subjective judgment.

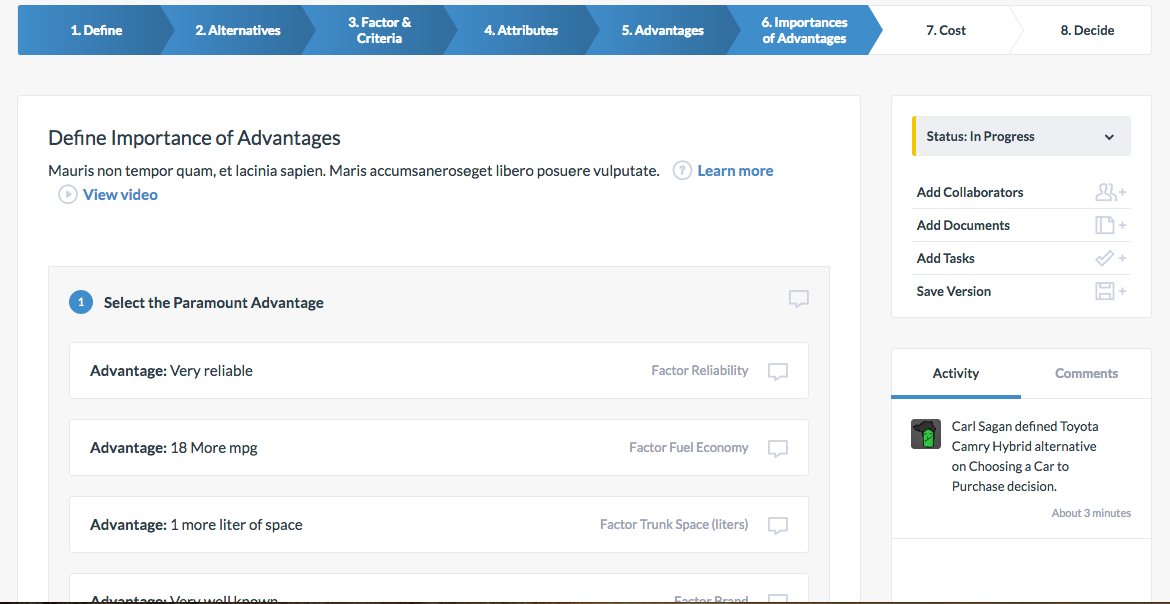

After determining the advantages of each alternative, the stakeholders need to decide the importance of each advantage (Step 6). Stakeholders need to explicitly state their preferences for the advantages and assigning a degree of importance to each advantage is therefore the first subjective task that requires stakeholders apply their subjective judgment.

Assigning a degree of importance to each advantage is done by first highlighting the most important advantage in each factor and then selecting the ‘Paramount’ advantage —the most important of the most-important advantages. CBA Tabular Method requires a common scale of importance to be used to minimize the likelihood of ambiguity in the decision-making process; the paramount advantage is used for this matter. The Paramount advantage takes the highest spot on the importance scale (usually 100 points) relative to the underlined attributes, each of which get assigned 0 points. Determining the paramount advantage is done by comparing the most-important advantages in each factor and selecting the most-important of these most-important advantages. The importance of the most-important advantage in each factor needs to be weighted and compared to the paramount advantage. Finally, a degree of importance is assigned to the remaining advantages relative to the paramount advantage. To conclude the process, the team adds up the importance of advantages for each alternative. The design alternative with the greatest total importance of advantages represents the best value solution.

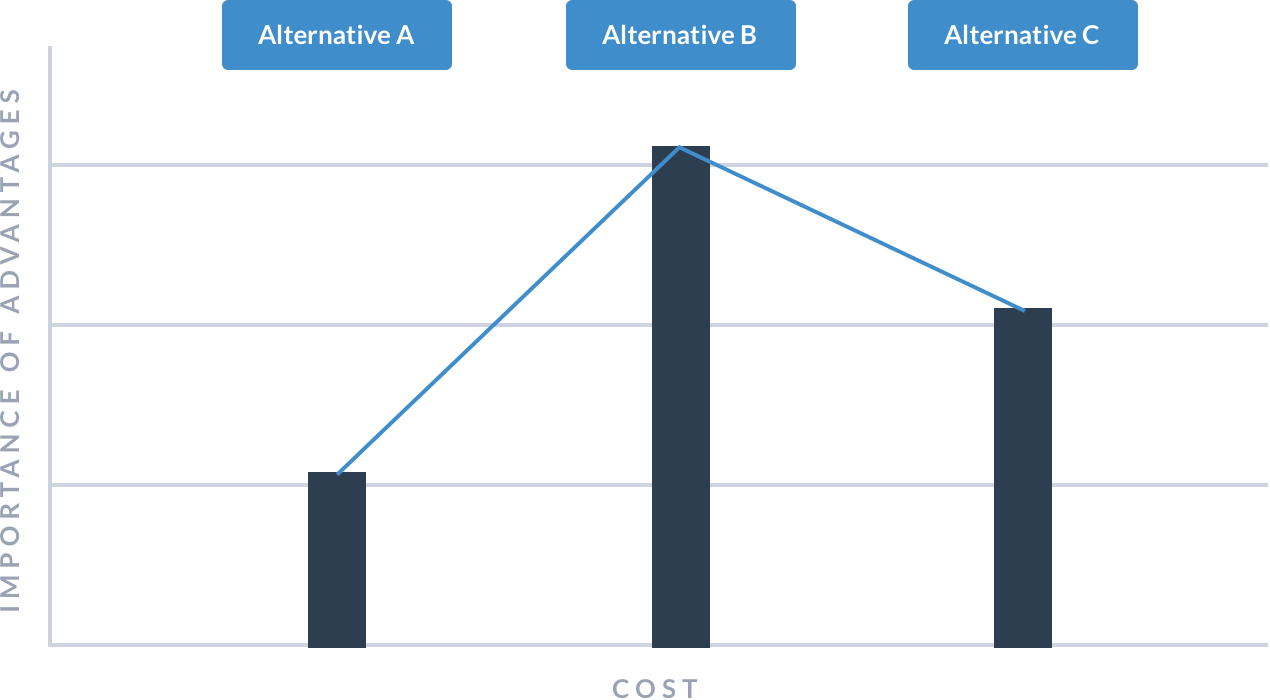

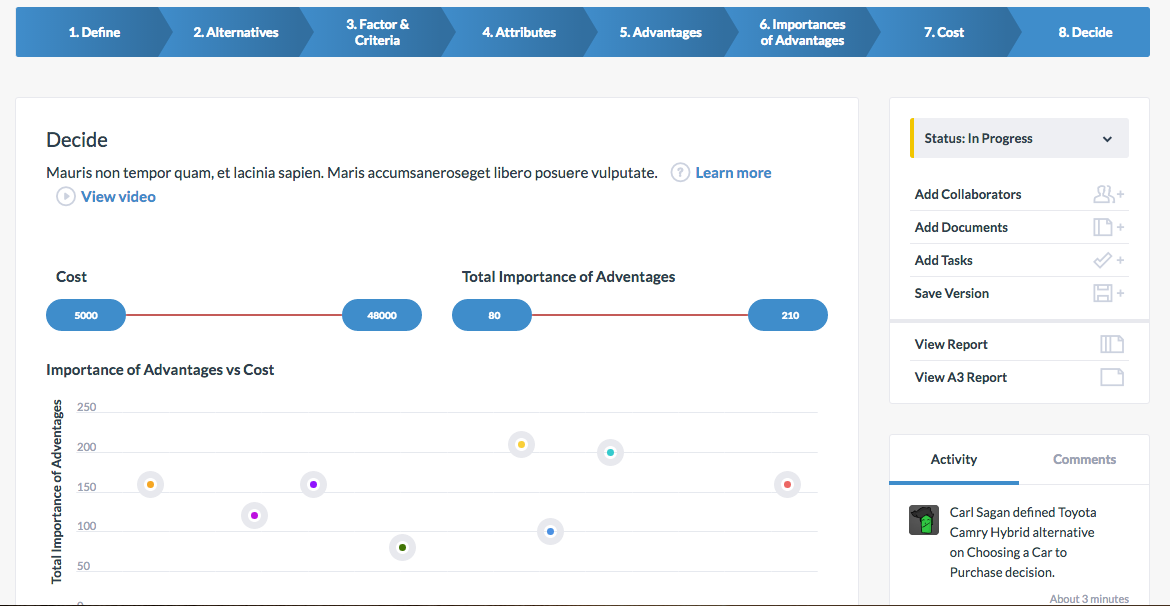

CBA Tabular Method considers cost separately from other factors. Cost is considered when two alternatives have different costs and the cheapest alternative does not have the highest total importance of advantages. According to Parrish (2009), money is described in the CBA system as “an official message that serves as a medium of exchange”. ‘Money decisions’ involve evaluating ‘increments’ between alternatives—an increase or decrease in cost from one alternative to another. For example, the figure below suggests that an increase in cost from Alternative A to B may be a desirable investment because the increment adds more importance of advantages. Meanwhile, an increase in cost from Alternative B to C is not desirable because Alternative C has a lower total importance. By separating cost from the importance of advantages, the CBA Tabular Method allows the decision-maker to make a conscious decision between the trade off between cost and value.

Cost vs. Importance of Advantages (Adopted from Lee 2012)

Cost vs. Importance of Advantages (Adopted from Lee 2012)

To learn more about CBA, visit our decision-making training, or attend one of our webinars.

Paramount Decisions is based on the CBA Tabular method, and help simplifies complex decision-making by dividing it into 8 steps ( the first step is to define your decision). In addition, Paramount Decisions includes a set of tools and feature to help you collaborate, learn and communicate your decisions. This includes the ability to generate reports, assign tasks, follow decisions status and create decision templates. Visit our product page for an overview over all features.

The Decision-Making steps in Paramount Decisions

The Decision-Making steps in Paramount Decisions

The Paramount Decisions process can be summarized by the following step:

Step 1: Define the decision name and define a set of tags to help you group similar decisions. You can also set the decision's objective, a due date, and specify a reminder.

Step 2: Identify alternatives and define all the alternatives likely to yield important advantages over other alternatives and that reflect values and goals you or the team wants to realize.

Step 3: Define factors to evaluate attributes of alternatives and agree on the criterion for each factor. Criteria can be either a desirable (‘want’) or a mandatory (‘must’) decision rule. Alternatives that do not comply with a ‘must’ criterion are not considered in the following steps. Adding a ‘want’ or ‘must’ criterion is optional; however, each factor must have at least 1 criterion.

Step 4: Summarize the attributes of each alternative. Summarizing attributes consists of listing objective facts or data to describe the attributes of each alternative, corresponding to the factors and criteria shown, thus anchoring the decision-making process to relevant facts. Attributes are inherent to an alternative, so this step avoids subjective judgment. Repeating factor by factor, determine which alternatives complies with the 'must' criterion, if you have defined such. Alternative that does not satisfy the 'must criterion' will not be considered in the subsequent steps of the decision-making process.

Step 5: Decide the advantages of each alternative. This is done by first selecting the least preferred attribute in each factor and then comparing each attribute to the least preferred attribute. After determining the advantages of each alternative, select the alternative that has the bigger advantage for each factor.

Step 6: Decide the importance of each advantage. This process is achieved through argumentations and discussions among team members. Assigning a degree of importance to each advantage is done by first selecting the ‘Paramount’ advantage —the most important advantage for all factors. Determining the paramount advantage is done by comparing the most-important advantages in each factor and selecting the most-important of these most-important advantages. The paramount advantage is used for setting a common scale of importance to be used to make advantages comparable. The paramount advantage takes the highest spot on the importance scale (100 points). Alternatives that do not have an advantage on one factor are not given points. Secondly, the importance of the most-important advantage in each factor needs to be weighted and compared to the paramount advantage on the established scale. Finally, decide the importance of each of the remaining advantages within each factor.

Step 7: Define the cost of each alternative. The cost is the price that must be paid in order to obtain an alternative and can be broken into several categories. Notice that the cost is treated separately with a clear distinction from the previous steps. This is because money is described in the CBA system as “an official message that serves as a medium of exchange”. Consider the first cost as well as lifecycle cost of each alternative.

Step 8: Decide which alternative you want to select based on how much you are willing to spend in order to obtain a certain level of importance of advantages. The total Importance of Advantages (the importance of advantages for each alternative added up) vs. Cost chart help you evaluate the best way of spending your resources. Evaluate ‘increments’ between alternatives—an increase or decrease in cost from one alternative to another — against the value (Importance of advantages) it provides, and make a decision.

When you have made a decision, you can generate a full report or a condensed summary of your decision in an A3 format to document and share your decisions with the remaining stakeholder. Visit our Product page to learn about the other feature.

For more info and instructions on how to use Paramount Decisions, please visit our User Guide.

Thanopoulos, Theodoros. "Lean Decision Making and Design Management for Sustainable Building Systems and Controls: Target Value Design, Set-Based Design, and Choosing By Advantages." Master Theises, Department of Civil and Environmental Engineering, University of California, Berkeley, 2012.